OPR: What is it and How Does it Impact Us?

Last year, I experienced an increase in mortgage payments. I’m sure that it’s the same with you too if you have mortgages to pay. Obviously, if you owe 6-figures in mortgages, your monthly installment would be increased in the hundreds. As for real estate investors who owe 7-8 figures in mortgages, the increment could be in the thousands or tens of thousands per month.

So, what is the root cause of this increment?

Answer: OPR.

In this article, I’ll explain what OPR is, its mechanism, and impact on us. You will discover how OPR affects our economy in terms of growth, inflation and as well as the strength (or weakness) of our Ringgit. I’ll end with a couple of pointers to discuss our take as investors on the subject of OPR.

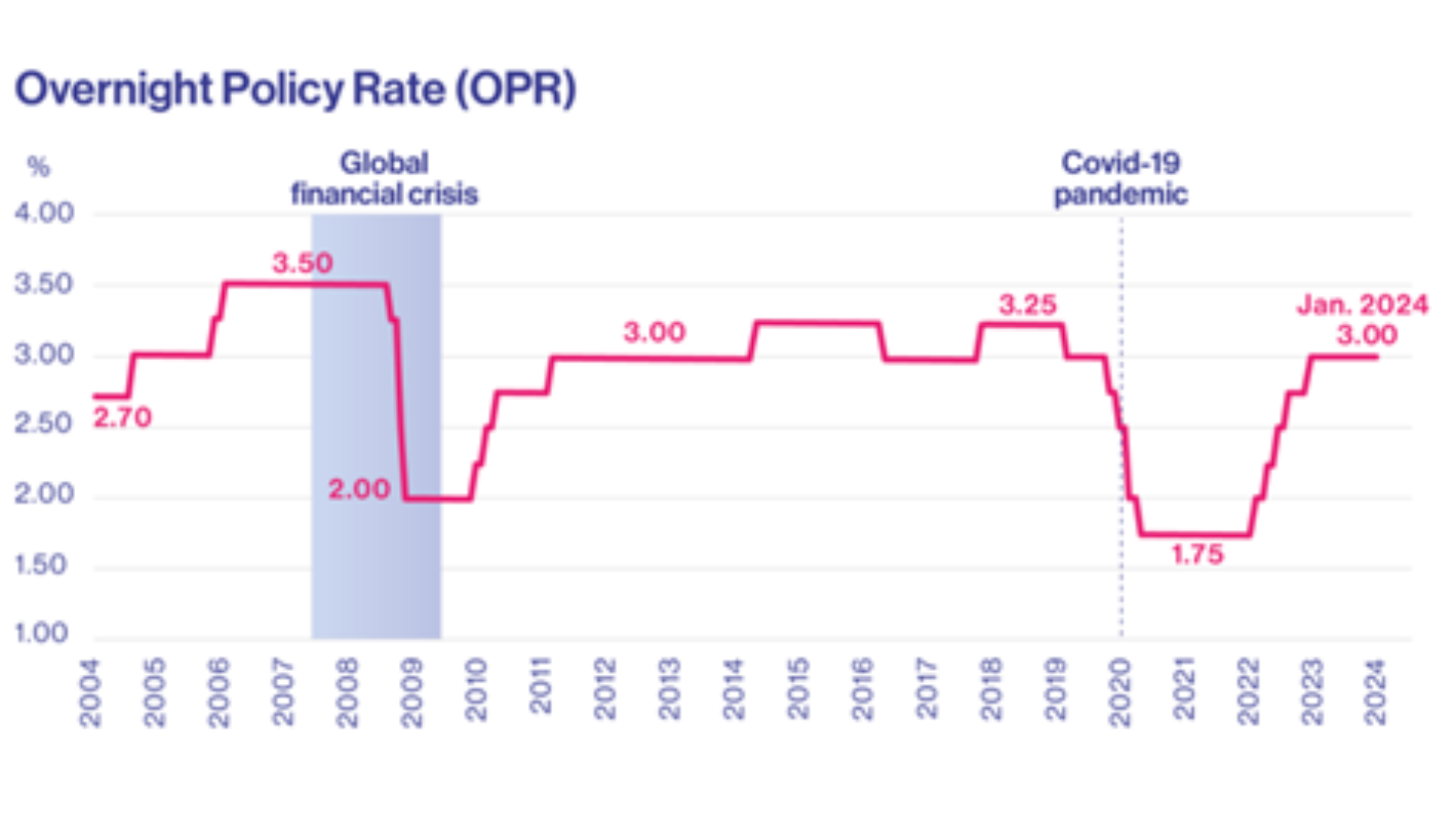

1. What is OPR?

OPR is an acronym of Overnight Policy Rate.

It is the interest rate set by Bank Negara Malaysia (BNM) via a committee which is known as the Monetary Policy Committee (MPC) on a bi-monthly basis. Here, the MPC comprises BNM’s Governor, Deputy Governors and external members, including those appointed by the Ministry of Finance (MOF). Today, we all could check OPRs and the rationales for these rates set for previous years (all the way back to 2004) via BNM’s official website.

Of which, we’ll learn that our OPR ranges between 1.75%-3.50% since 2004.

Source: BNM

The MPC’s role in setting OPR is hugely important as it influences both our local deposit and lending (and financing) rates. Such will in turn impact inflation rate, economic growth rate, and the strength of our Ringgit. Let me explain:

2. How to Spur Economic Growth?

Let’s say BNM chooses to lower OPR.

By lowering lending and financing rates, the cost of borrowing decreases. This opens a gateway for business owners to strategically leverage debt to expand their operations—whether that's opening new outlets, funding ambitious projects, or bringing fresh talent on board. As a result, more jobs are created, chipping away at unemployment rates and putting more money into the pockets of the populations. This influx of income enhances their capacity to spend, borrow, and invest, setting in motion a virtuous cycle of prosperity. With a reduced OPR, the message is clear: it's time to boost our spending, borrowings, and investments.

In such a climate, the appeal of deposit rates diminishes. This subtle shift nudges people away from the traditional nest-egg approach, encouraging them not to let their cash sit idle.

3. How to Curb Inflation?

Yet, maintaining a low OPR for an extended period can inadvertently fuel inflation, pushing the cost of living higher. This surge affects everything from our daily expenses to the broader markets, including stocks and real estate, which might become excessively buoyant.

To mitigate this, Bank Negara Malaysia (BNM) takes a proactive stance by elevating the OPR. Such adjustments are pivotal as they lead to an increase in lending and financing rates, making borrowing more expensive. This shift naturally cools down the propensity to spend, borrow, and invest, effectively applying brakes to the economy's overheating tendencies. The ultimate goal? A steady pace of economic growth with inflation kept firmly in check.

In this adjusted scenario, the allure of Fixed Deposits (FDs) becomes more pronounced. With higher deposit rates on offer, many find it a prudent choice to allocate their funds into FDs, seeking to benefit from the improved returns.

4. How Does OPR Affect the Strength of RM?

Now, here is a question.

Supposedly, you want to place RM 100k into a FD. There are two banks that you can choose from. Bank A offers 3% and Bank B offers 5% for their respective FD. Thus, which of the two banks would you choose to place your money with?

Obviously, you’ll choose Bank B as its interest rate is higher at 5%.

What if this is applied to BNM and the US Federal Reserve (Fed)?

Since 2022, BNM has raised OPR from 1.75% to 3.00% presently. Meanwhile, in this period, the Fed had raised its rates from 0.50% to 5.50% presently. Today, it is obvious that BNM is likened to Bank A (3%) and the Fed is Bank B (5.5%). This causes trillions to flow into the United States as many want to earn higher rates for their monies. When that happens, the US Dollar becomes highly in demand, thus, causing it to strengthen against our Ringgit.

Source: Google Finance

When the US Dollar strengthens against our Ringgit, imports become expensive and this also causes inflation to rise. In contrast, our exports to trading partners overseas would become cheaper and more competitive.

Thus, the weakening of our Ringgit may not necessarily be a bad thing. To us, as individuals, it all depends on how we view and manage this situation.

Perhaps, you might wonder:

Could BNM Strengthen our Ringgit by Raising OPR?

Sure, it can. But, the price is a slower growth in our nation’s economy. It means: higher borrowing costs, higher unemployment rates, less competitive exports and less incentives from our government due to lower tax revenues.

What if BNM Chooses to Lower our OPR?

As discussed, this would bring economic growth in our nation. But, we could be experiencing inflation as a result of a weak Ringgit.

Thus, the MPC’s role is to consider all these factors when setting OPRs. It is vital to strike a fine balance between spurring economic growth, controlling inflation and keeping the strength of our Ringgit among global currencies.

5. OPR’s Impact to Investors

“OPR is going up/down. Is it a good/bad time to invest in stocks/properties?”

As investors, we choose our investments based on fundamentals, be it stocks or properties. Stocks and properties that are fundamentally strong should bring us recurring income in times when OPR is up and down. Hence, it is not a question of buying or selling any investments based on OPR fluctuations.

But, OPR can influence our decisions when it comes to funding our investments and preserving our investment capital.

For instance, as an investor, I’ll put more cash into my flexi-loan accounts, when OPR rises. This allows me to save on interest costs while waiting for good stocks/property deals to capitalize on. But, when OPR declines, there is less incentive for me to do so. I'd rather invest globally to obtain better returns for my capital.

Conclusion: Boosting ROI from ASB Using ASB financing.

Note: This is applicable for Bumiputeras (Bumis) only.

For Bumis, there is an option to finance ASB investments with ASB financing. This is a viable method to obtain higher ROI from ASB due to leverage. Typically, if one earns good income, has strong credit and RM 100k in capital, he can choose:

Option A: Invest RM 100k in ASB with his own money.

Option B: Invest RM 100k in ASB with his own money, plus financing for ASB investment say another RM 100k.

Assuming that ASB could deliver 5% in annual dividend yields, he would receive 5% in dividend yield with Option A. But for Option B, he would achieve a much higher return with the leverage. To check out the actual return calculation for investing in ASB using ASB financing:

Link: Webinar - How to Generate 10+% p.a. From Your ASB Investments?

As long as the dividend from ASB is higher than the cost of financing, it is ideal to use a financing to invest in ASB when OPR is low. To Bumi investors, using ASB financing allows investors to enhance liquidity and actual return despite investing in the same vehicle. Thus, it is advantageous for Bumi investors to be aware of this in order to be more efficient in building long-term wealth.