Year-End Review & Financial Planning for 2025

Time flies. In less than two weeks, we would usher in the year 2025.

Beyond festivities, I find this season ideal to reflect and plan our finances. It is helpful to have an idea on how we fare in 2024 and how we can progress in our financial lives in 2025 and beyond.

But, what if you are new to planning your finances? If that is you, no worries. In this article, I’ll be sharing 3 major factors to focus on when reviewing your finances. These factors are most useful if you are in the working class as they may position you towards a much prosperous, purposeful, and fulfilled life. The 3 factors are as follows:

Factor 1 - Income Growth

Income growth is critical to wealth building. The more we earn, the more we can save and invest to build wealth. So, the first step to review our finances is to know if we increased our income for 2024 as compared to 2023. The second step is to know the factors that contribute to our income for the present year.

This is crucial as different people earn different types of income. For instance, some earn a fixed salary from routine jobs. Meanwhile, there are others who earn variable income from the results, impact and value of their works delivered to their clients and bosses.

Often, the one who earns variable income has more potential to grow income over the other that earns fixed income. This is because people who earn variable income can increase their income more easily and substantially by making minor improvements progressively.

Here’s an example.

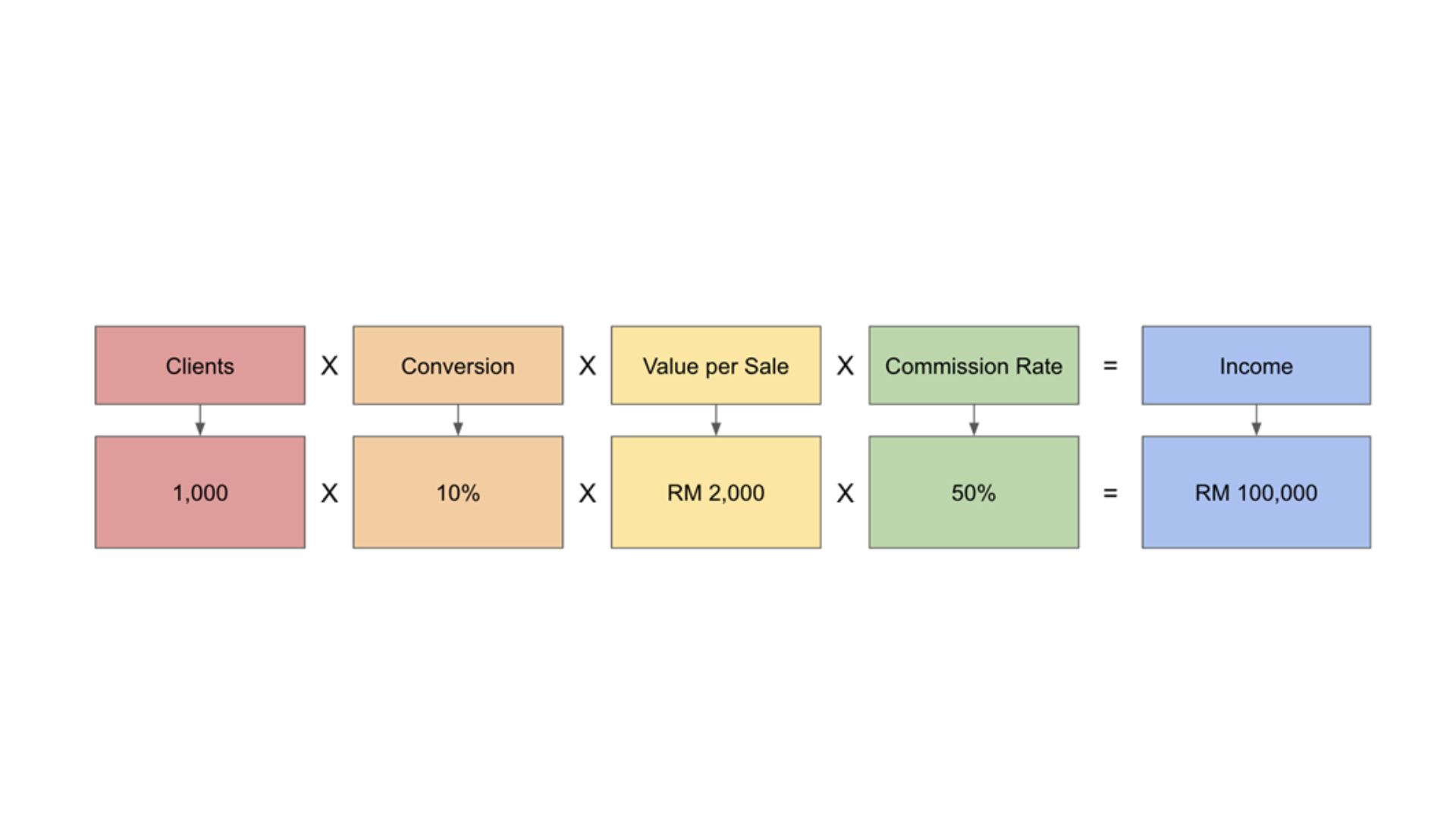

Let’s say you are into sales. In 2024, you met up with 1,000 clients, converted 10% of the clients to obtain 100 sales, which are worth RM 2,000 each. So, you’ve generated RM 200,000 in sales in 2024. Of which, at 50% commission rate, your income is RM 100,000 in 2024. In this case, as a sales professional, the formula to your income is as follows:

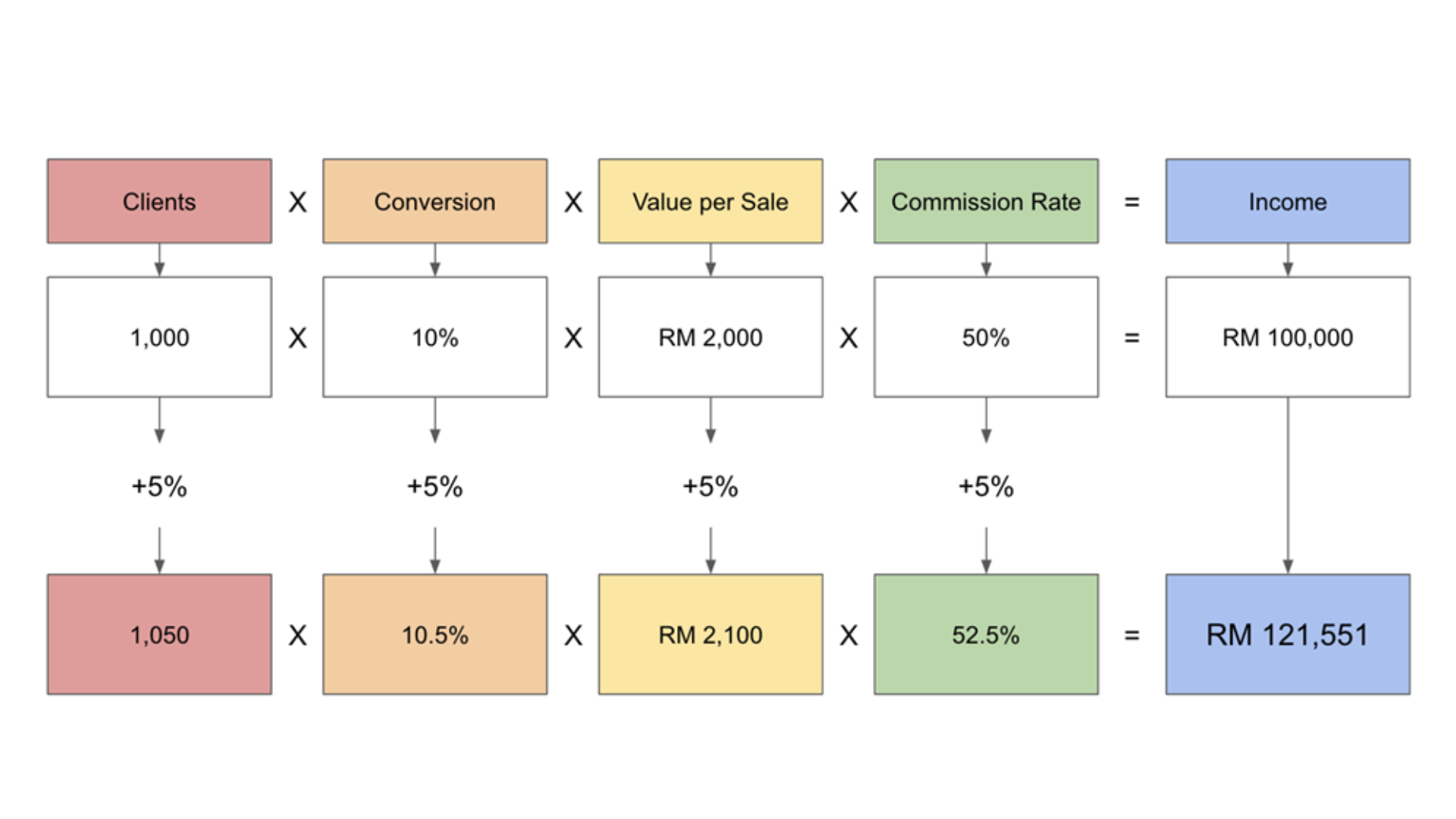

So, what can you do to enhance your income by 20% to RM 120,000 in 2025?

Could you meet 20% more clients to raise your income by 20%? Sure, you can. However, it may be possible that you’ll face a career burnout, especially if you’re raising your workload by 20% in 2025.

Alternatively, imagine you could just:

1. Meet 5% more clients (You meet 1,050 clients in 2025).

2. Improve conversion rate by 5% (You secure 10.5 sales after meeting 100 clients)

3. Raise value per sale by 5% (Value increased from RM 2,000 to RM 2,100)

4. Raise commission rate by 5% (Commission rate increased to 52.5%)

Guess how much you would earn in 2025?

The answer is RM121,551, which is a 21% increment from this year.

Impressed? So, how could you convert more, raise your value per sale and commission rate? Is it always about working harder? Not quite. I believe the above is attainable if we can sell, market and communicate our value better to our clients and bosses. Such requires training and practice over time. These could be one of your enhancement strategies to grow your income in 2025 and beyond. If you can do so, let’s move onto:

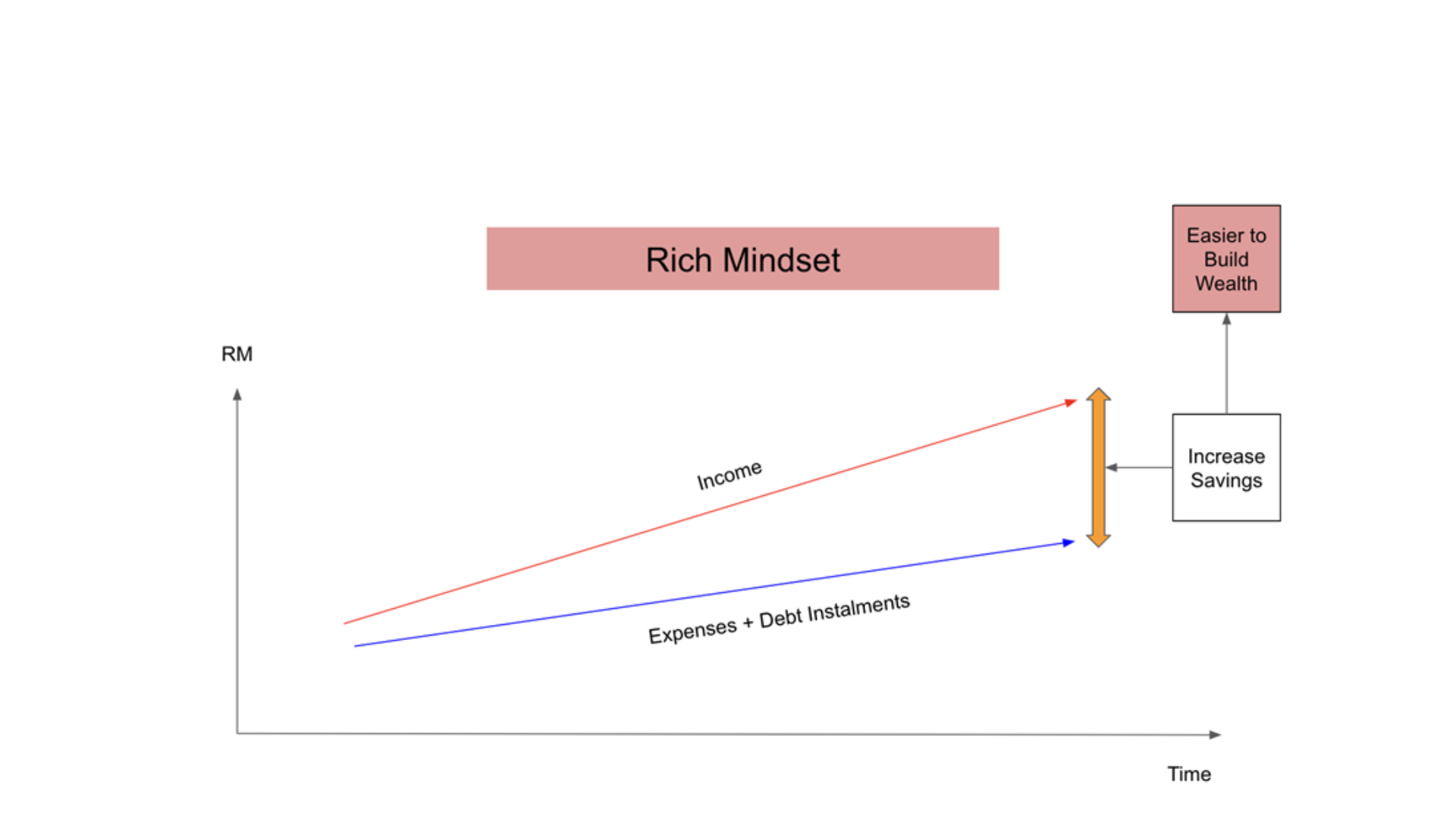

Factor 2 - Savings Growth

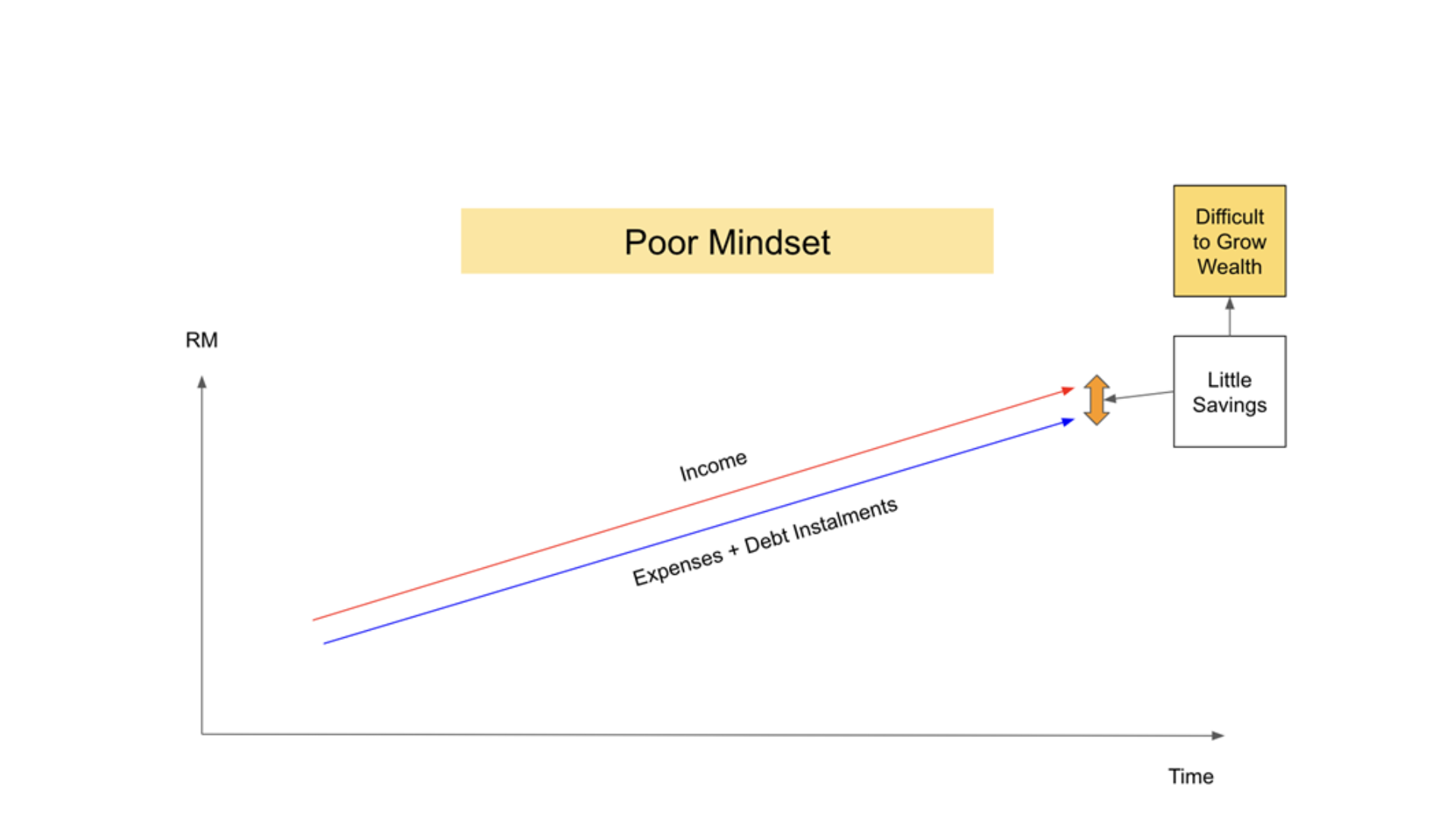

As mentioned, one can save and invest more upon earning more. But, that is often not the case. This is because many hold a belief that they would spend and borrow more upon earning more.

Sure, while it is true that we spend and borrow more upon earning more, the difference between one that is progressing and the other who is regressing lies in the ability to control such increase in expenditures and create a larger buffer between income and expenses.

Normally, the rich can create a larger buffer and raise capital for savings and investments. As for the poor, they would struggle to do so as they tend to have expenses that match or exceed their income over time. As a result, the rich could become richer while unfortunately for the poor, they would become poorer.

Which of the two is more reflective towards your financial life? If it is the latter, that’s good. But, if you have been:

1. Spending RM 4k a month when you earn RM 4k a month

2. Spending RM 6k a month when you earn RM 6k a month

3. Spending RM 20k a month when you earn RM 20k a month

4. and so on and so forth.

It is difficult for you to build wealth.

If you like a change, you have to first change your mindset and belief about wealth. Once you’ve done so, a more practical enhancement strategy is as follows:

1. Increase your income to RM 10k a month.

2. Maintain your spending at RM 8k a month when you earn RM 10k a month.

3. Continue to spend RM 8k a month when you earn RM 12k, RM 14k ... a month and beyond.

4. Use the amount saved to either invest or reduce debt.

If you can do so, we can move onto:

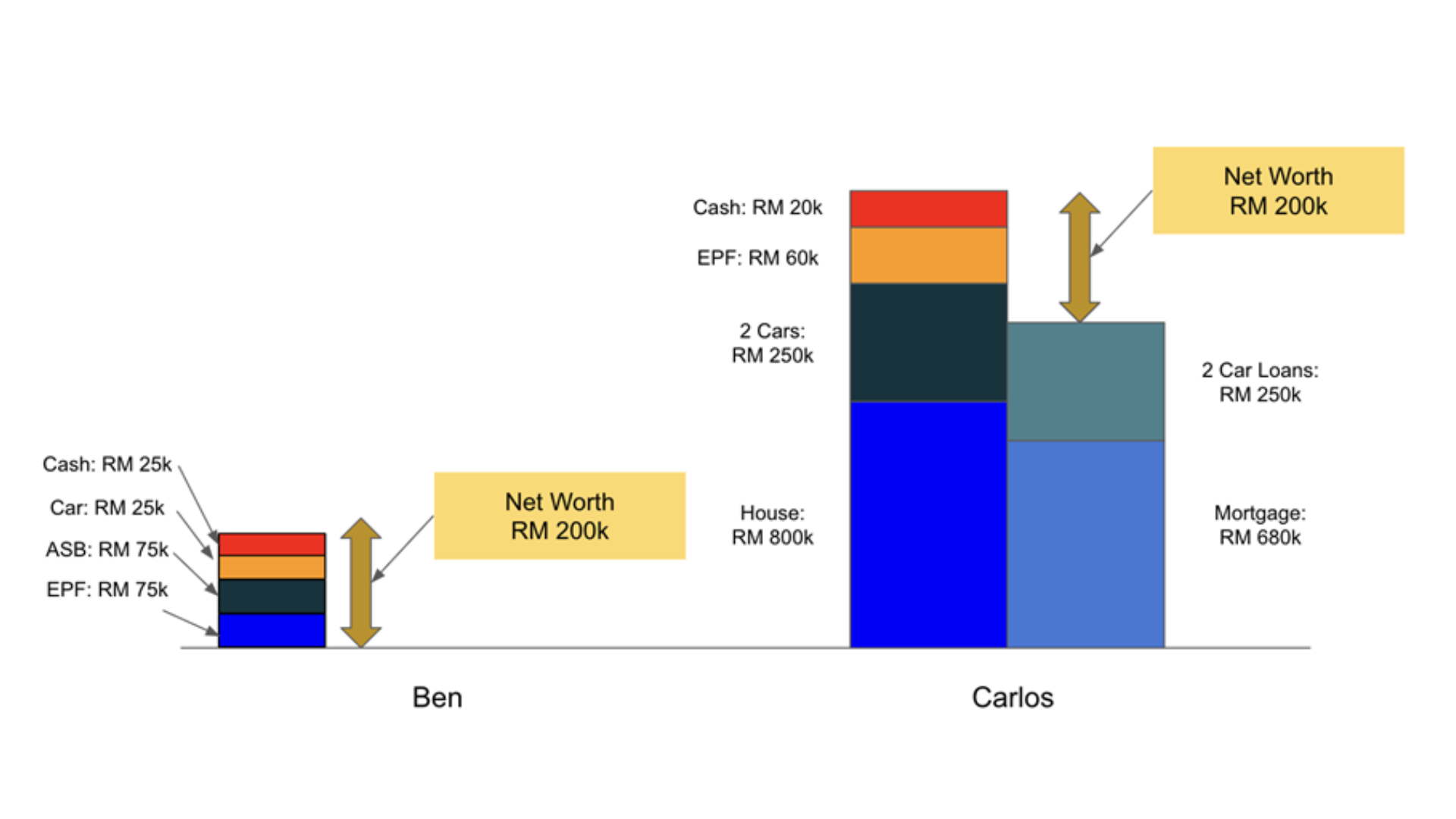

Factor 3 - Net Worth Growth

For a start, net worth is calculated by deducting all liabilities from his or her assets. For instance, if you own RM 1 million in assets and owe RM 700k in liabilities, your net worth is RM 300k. The questions are: “Had you grown your net worth in 2024 as compared to 2023?” and also, critically speaking, “What is the current composition of your net worth?”. This is key as the composition of your net worth could tell you if you are in position to attain wealth or otherwise.

Take two friends, Ben and Carlos, as an example.

Both earn RM 8k a month and have a similar net worth of RM 200k.

For Ben, he owns RM 200k in assets which consists of RM 75k in EPF, RM 75k in ASB, RM 25k in cash and a fully-paid car worth RM 25k. Ben is debt-free.

For Carlos, he owns RM 1.13 million in assets that comprise a RM 800k home, two cars that are worth RM 250k, RM 60k in EPF, and RM 20k in cash. Carlos owes RM 930k in liabilities that are inclusive of a RM 680k in mortgage and RM 250k in car loans.

So, who is in a better position to grow his wealth? Is it Ben or Carlos?

The answer is Ben.

Take a look at their net worth composition. Ben has more productive assets than Carlos, despite Carlos having more assets than him. Ben earns dividends from RM 75k in EPF and distributions from RM 75k in ASB. Carlos has RM 60k in EPF which is income productive. However, Carlos is the one who owns RM 1.05 million in consumption assets (1 house and 2 cars) that do not generate income. The only way for Carlos to grow his net worth significantly is for his house to appreciate in price and such quantum exceeds the quantum of depreciation of his two cars.

Also, it is possible for Ben to save and invest more as compared to Carlos who is “chained” with debt installments. Carlos can grow his net worth bit by bit as he services his debt instalments. In Ben’s case, he is free to acquire and accumulate assets to grow his wealth.

So, which of the two balance sheets reflect your current situation?

If yours is like Ben, that’s great. Your enhancement strategy is to continue on the good work and keep on investing in productive assets. But, if yours is like Carlos, little could be done to improve and enhance your net worth provided you are willing to sell off your house and two cars and pay off these debts. Sure, you can keep these “assets” and raise your income. But, that strategy can be slow in terms of wealth building as it takes more time to raise income.

Conclusion:

We can review our finances by measuring the growth of our income, savings and net worth. This allows us to have a picture of where we stand financially. Of which, we may strategize and make plans to elevate our financial lives. In reality, the fastest way to build wealth is to have all of the 3 factors working in unison. This means, income growth should lead to savings growth which shall lead to growth in productive assets and ultimately, leading to growth in our net worth. Beyond this review, it is helpful to have a habit of reviewing our finances on a monthly basis. I’m confident that if we keep track of our finances and work towards our goals, we’re positioning and increasing our chances to live prosperous and fulfilled financial lives in 2025 and beyond.