Digital Bank: How Does It Benefit Us as Consumers?

On 31 December 2020, Bank Negara Malaysia (BNM) issued the official licensing framework for digital banks in Malaysia. It is a step forward towards providing efficient banking services to both the unserved and the underserved communities in our nation. With this framework, it has started the race among interested corporations to apply for its licence with BNM.

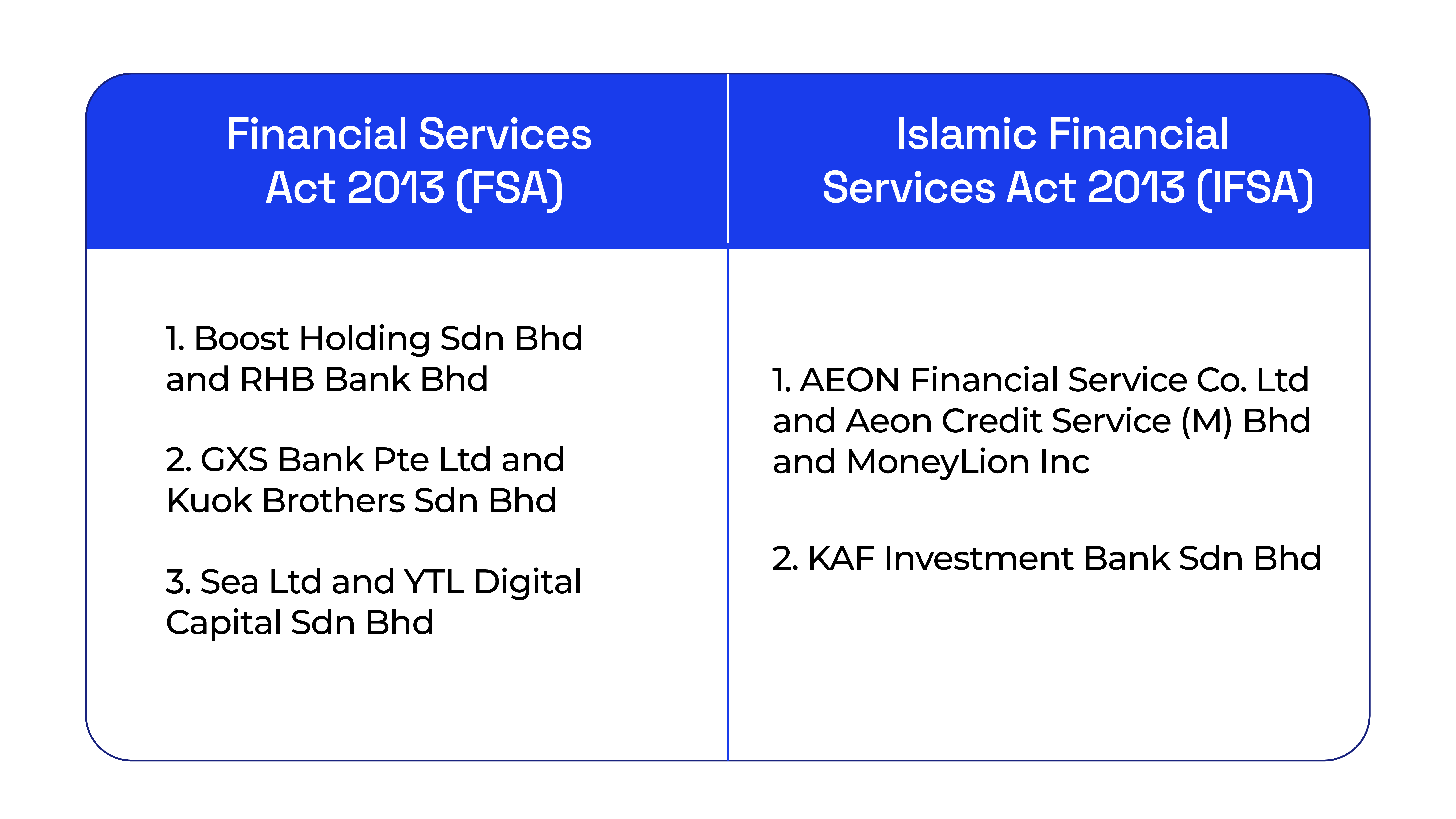

Six months later, on 2 July 2021, BNM announced that it received 29 applications for the licence to operate a digital bank. Subsequently, on 29 April 2022, BNM announced that it has granted to five successful applicants the licence to operate digital banks in Malaysia. These applicants are:

Currently, three digital banks were launched. They are GX Bank, Boost Bank and Aeon Bank. In this article, I’ll share what a digital bank is and make a list of benefits for using it.

What is a Digital Bank?

A digital bank is a bank operating digitally. It allows us to open accounts, deposit, store, transfer, and soon, borrow money online. There are no bank branches to visit, no bank officers to meet face-to-face, no queue and no ATMs. If help is required, a digital bank would respond via email, phone or a Live Chat at our convenience. Banking is no longer restricted to weekdays from 9am to 4.30pm. All of us can do banking 24/7 and anywhere as long as we are digitally connected.

With such features, I believe we all can imagine some immediate benefits from digital banking.

1. Efficiency

Right now, most conventional banks are focused on opening branches in cities and major towns where they can turn a higher profit. If you live around the Klang Valley, you’ve probably noticed that you’re never far from 5-10 banks, both local and international, giving you plenty of options for your banking needs.

But for those in smaller towns or rural villages, it’s a different story. If you’ve ever travelled to these areas, you’ll know how hard it can be to find even a single bank branch. Often, villagers have to travel tens of kilometers just to do something as simple as depositing money or paying a bill. It’s a major hassle.

This is where digital banks are a game changer. With just a smartphone or laptop, people in these underserved areas can access full banking services without ever leaving home. It’s not just more efficient—it’s a step toward greater financial inclusion for all Malaysians.

2. Safety

I believe the most fundamental capability of any bank is to keep cash and transactions safe. The custody of wealth is the foundation of trust between banks and customers like us. If such trust is breached, all of us would keep our money at home. That would be catastrophic.

Typically, a digital bank is equipped with advanced safety features. They would include its ability, efficiency and precision of recognising each customer based on his or her device. This would be possible through biometric authentication, 2FA and card lock or unlock functions. Presently, as a result of heightening fraud and scams, we can protect ourselves from financial loss due to fraud, scams and unauthorised transactions with insurance.

For example, GX Bank offers “Cyber Fraud Protect”, which is an insurance product underwritten by Zurich that allows customers to claim up to RM 5k, RM 10k and RM 20k for a premium of RM 1, RM 2 and RM 4 per month. This provides further assurance to customers when it comes to its ability and commitment to keep money safe and be a good custodian of wealth.

3. Perks

Digital banks need to incentivise “the Rakyat” to open accounts and deposit money with them. If not, most of us would probably keep our money in conventional banks.

The obvious perk offered by the three newly launched digital banks is daily interest rates. Today, we can earn 2%-4% in interest rate per annum for our deposit. Although the rate is similar to FD offered by conventional banks, digital banks have no lock-in period. If depositors place money in FD and uplift them before they expire, depositors would forfeit their interests. It is not the case to depositors who place money with digital banks as their interests are credited on a daily basis.

In addition, the three digital banks would offer rewards on spending. To name a few, they include the following:

But that’s not all. GX Bank users on social media have reported a major perk when withdrawing cash overseas. The GX Bank card offers better foreign exchange rates and lower charges compared to conventional debit cards. This means you get more for your money while travelling abroad, making it an appealing option for frequent travellers.

4. Coming Soon: Micro-Financing

Could we apply for a home mortgage from digital banks in the near future?

Personally, I don’t think this will happen at least for the first 3-5 years in operations. For now, the amount of assets a digital bank could have is capped at RM 3 billion. If it offers mortgages to the public and let’s say, the average mortgage size is RM 500k, the maximum borrowers that they’re able to lend to would be 6,000. Also, if these banks are raising funds from depositors by offering interest rates at 2%-4% per year, could they offer better mortgage rates than conventional banks and be profitable?

Take Maybank and Public Bank as examples.

In 2023, Maybank had RM 1.03 trillion in assets. Public Bank had RM 510.6 billion in assets. So, at that scale, conventional banks would focus on lending huge loans at competitive rates. These loans would bring more impact to the banks’ bottom line.

Instead of big loans, digital banks will most likely focus on small loans (micro-financing). Today, I find that micro-financing is expensive. Their interest rates are high and could go into double-digit per annum. Now, with digital banks, they could offer some competition to this market and hence, bring down the interest rates charged on these small loans. This would offer greater liquidity to a huge community of local traders, small business owners and customers.

With cheaper micro-financing, a hawker can fund the set-up costs of her stall and earn her family a living. A local trader can do more trade and grow profits from using small loans to purchase his inventories from his suppliers and fund marketing activities.

This will enhance the money flow, especially among the B40 and M40 communities in our nation and so, fulfil the original intent to serve the unserved and underserved in Malaysia. Collectively, I believe this could reduce poverty and elevate our nation’s economy.

Conclusion:

It’s clear that digital banks are more than just a convenient alternative to conventional banking. They’re set to play a vital role in making banking more efficient, inclusive, and accessible to all Malaysians. While digital banks are still in their early phases, the benefits are already becoming apparent. Over the next 5-10 years, we’ll truly see how they revolutionize the way we manage our money.

So, why not give digital banking a try? After all, the future of banking is already here, and it’s as easy as a tap on your screen.