Is ASB Still Relevant as an Investment Option?

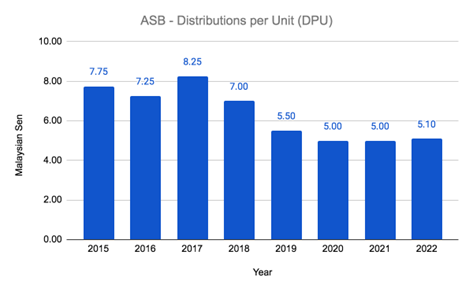

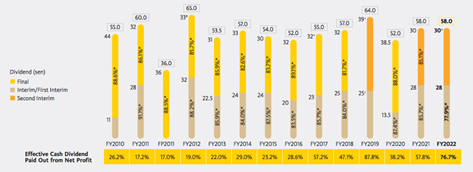

Launched on 2 January 1990, Amanah Saham Bumiputera (ASB) has remained a popular vehicle among Bumiputeras to earn competitive yearly returns while at the same, preserving capital. Under the stewardship of Permodalan Nasional Berhad (PNB), ASB has historically disbursed appealing annual dividends. However, a noticeable shift occurred in the epoch stretching from 2020 to 2023, during which the distribution per unit (DPU) witnessed a contraction, hovering over the margin of 5+ sen annually throughout this four-year timeline.

Source: ASB

Thus arises the pivotal query: "Does ASB retain its merit as a sound investment choice?"

It warrants a closer inspection.

In this article, I shall share some insights crucial for every ASB unitholder's awareness. These findings will aid us in ascertaining the current investment viability of ASB.

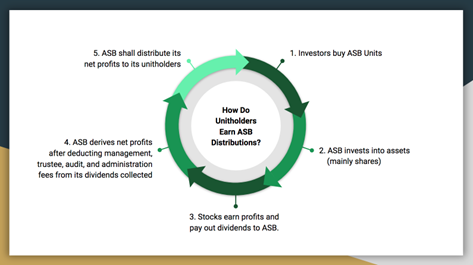

1. How Do Investors Earn ASB Distributions?

As investors, it is key to know how ASB earns income as DPUs do not just simply appear magically out of thin air. There are sources to your DPUs and simply put, here is the mechanism of how annual DPUs from ASB is derived:

Investors invest capital to buy ASB units.

ASB invests your capital to buy assets (mainly shares).

Stocks earn profits and pay out dividends to ASB.

ASB deducts expenses like management, audit, trustee & admin fees.

After such deductions, ASB derives its annual net profits.

These net profits shall be distributed to ASB unitholders annually.

As such, this leads us to our next point, where we’ll discuss what ASB invests in.

2. ASB’s Fund Composition

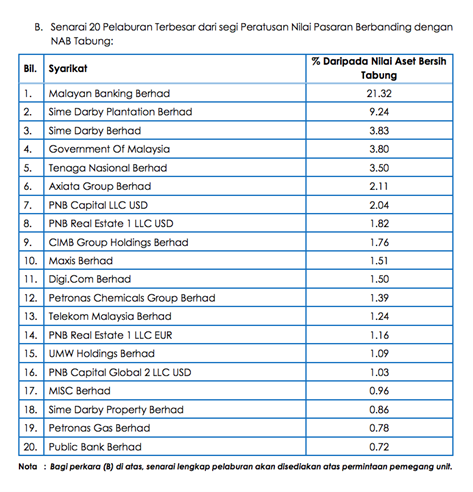

ASB has released its annual reports from 2016 to 2022 on its website. Of which, we could easily check out ASB’s 20 largest investments on an annual basis. So in 2022, the 20 biggest investments ASB held on in proportion to the net assets of its fund are reported as follows:

Source: ASB’s Annual Report 2022 (Page 4)

Here are some observations:

- The 20 largest investments have accounted for 61.66% of the fund’s net assets in 2022.

- Most of them are invested in stocks listed on Bursa Malaysia.

- Malayan Banking Bhd (Maybank) is ASB’s single biggest investment as it accounted for 21.32% of the fund’s net assets in 2022.

3. How Did Maybank Perform as an Income-Generator?

Your annual DPUs is dependent on income-generating abilities of stocks held by ASB for the long-term. If these stocks earn more profits, they may pay out more dividends to ASB, which in turn, will allow ASB to pay more distributions to you. But, if these stocks earn less profits, then, ASB would receive less dividends and thus, would pay out less distributions to you.

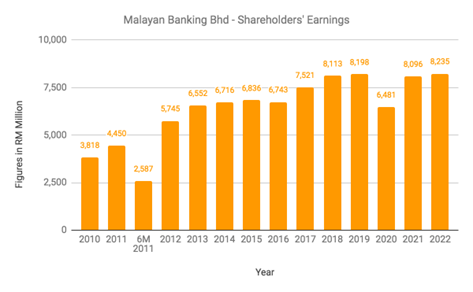

But since Maybank is ASB’s single biggest investment, its financial results will be most impactful to your annual DPUs.

From Maybank’s annual reports, we would find that:

- ASB is the largest shareholder of Maybank with 32.58% shareholdings.

- Maybank has delivered consistent growth in earnings. It increased from RM 5.75 billion in 2012 to RM 8.24 billion in 2022.

- Maybank has paid out 50-60 sen in dividends per share (DPS) in the last 10 years since 2013.

Source: Maybank’s Annual Reports

Source: Maybank’s Annual Reports 2022 Obviously, if you choose to dig deeper into other stocks owned by ASB, like Sime Darby, Tenaga Nasional, Axiata, CIMB, Maxis, and so on, you will find that their financial results are different. Some have made consistent profits, while some are less consistent in generating profits.

Typically, as a stock investor, stocks that deliver consistent earnings growth over the long term tend to achieve sustainable capital growth in the long run. But, in the case of stocks that don’t, their stock prices tend to fall in the long run. So, if you are a stock investor like myself, there is an element of price volatility, which is great if you are savvy but a total nightmare if you aren’t a savvy investor.

As such, if you wish to avoid price volatility but are interested in participating in the stocks’ income for the long run, ASB would be a suitable vehicle as the fund is a fixed-price income fund. There is no concern for market ups and downs and volatilities as you are not participating in capital gains or losses as an unitholder of this fund.

4. But, Won’t ASB Sell Off its Investments?

PNB, ASB’s investment manager, has the discretion to make decisions: buy, hold or sell any investments within the fund’s mandate. For ASB, such assets include:

Securities listed on Bursa Malaysia (equities)

Unlisted securities

Fixed income

Money market instruments

So, the question is: “Would ASB’s fund composition remain similar tomorrow as compared to today?”. Or, would ASB be a fund that holds Maybank, Sime Darby Plantations and TNB today but will totally change its portfolio tomorrow?

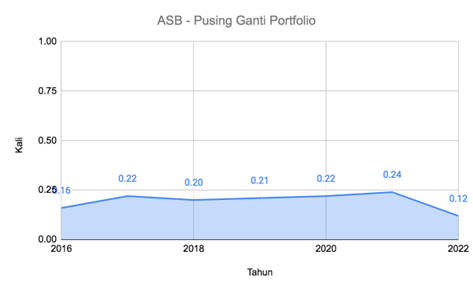

While there is no guarantee, as unitholders, there is a metric which can be used to assess the investment behaviour of a fund. The metric is known as “Portfolio Turnover Ratio” or PTR. In Bahasa Malaysia, it is Pusing Ganti Portfolio.

A fund that has low PTR is one that trades less and tends to hold onto assets for a longer term. A fund that has high PTR is one which trades more actively and is likened to a trading portfolio. For ASB, it has kept its PTR at relatively low levels:

Source: ASB

This is further evidenced by ASB’s fund composition in 2016-2022, which shows that ASB kept most of its 20 largest investments in its portfolio in that period. In this case, we could tell that ASB has the tendency to retain what it had invested in its portfolio for the long-term. This means, your DPUs shall continue to come from its 20 largest investments as revealed earlier.

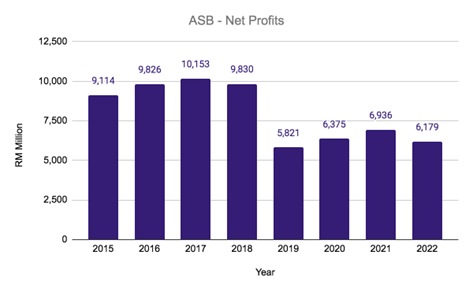

5. Why Did ASB’s Distributions Fall in 2019-2022?

Simple. The fall in DPU was due to its fall in net profits. From its annual reports, ASB has reported a decrease in net profits from RM 9-10 billion in 2015-2018 to RM 5-6 billion in 2019-2022.

Source: ASB’s Annual Reports

The reasons for such declines are as follows:

- Lower realised gains from divestments in 2019-2022 than 2015-2018 of RM 2-3 billion. It is key to note that divesting gains tend to be one-off & not exactly a source of income to depend on if you are looking to make, earn or receive recurring income from an investment.

- Lower interest income due to falling interest rates in 2019-2022.

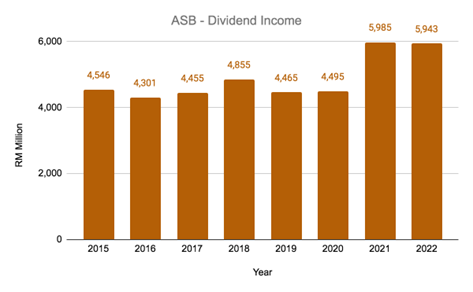

The primary source of income, which is dividends, has held up well where it has increased from RM 4+ billion in 2015-2020 to around RM 6 billion in 2021-2022 as shown below. I think the amount of dividend income earned by ASB would be a better measure of ASB’s ability in paying out distributions to unitholders.

Source: ASB’s Annual Reports

All in all, based on ASB’s 4-year track record of generating around RM 6 billion a year in net profits, it would pay out at least 5 sen in annual DPU. This works out to be 5% per annum in distribution yield.

Conclusion:

Upon further studies, it is evident that the fall in DPUs in 2020-2023 isn’t due to a fall in dividend income received from its investments but rather an absence of realised divesting gains in that period. Based on its past performances, ASB had delivered competitive returns while preserving capital and thus, had fulfilled its objectives. Moving forward, ASB would be relevant for investors who wish to:

Avoid / reduce price volatility in their overall portfolios.

Earn better returns than local FD rates.

In a landscape of fluctuating financial tides, ASB stands as a beacon for those seeking stability in their investment horizons.