5 Tips to Achieve Financial Freedom in Malaysia

One of my favourite quotes from Morgan Housel’s The Psychology of Money goes like this: "Controlling your time is the highest dividend money pays."

Just picture it—waking up each day with the freedom to choose how you want to spend your time, where you want to be, and who you want to be with. That kind of freedom is priceless and is the ultimate reward of financial independence.

But what if your reality today feels like the typical rat race? You’re working hard but not really getting ahead, and life seems like an endless cycle of paying bills. Is financial freedom even achievable, or is it just a far-fetched dream?

I’ve been there. I come from humble beginnings, and in my 20s, I started educating myself about personal finance and investing.

I realized that achieving financial freedom isn’t just possible—it’s attainable if you understand what it looks like, have a plan, and stick to it. Today, I’m fortunate to say that I’m financially free.

So, here are five tips that helped me get there, and I hope they can help you fast-track your journey to financial freedom too.

Tip 1: Understanding Your Financial Freedom Ratio

The journey to financial freedom starts with understanding a simple formula:

Financial Freedom Ratio =

Current Assets / (Monthly Cash Outflows -Passive Income)

This formula breaks down into three key components: current assets, monthly cash outflows, and passive income.

Current assets are those you can quickly convert to cash within a year. Think cash in the bank, stocks, ASB, unit trust funds, ETFs, REITs, and even cryptocurrencies.

On the other hand, assets like cars and real estate fall under non-current assets—they're valuable but take more time and effort to turn into cash.

Monthly cash outflows include everything you spend on living expenses and any monthly debt repayments.

Passive income is the money that keeps rolling in without you actively working for it—interest from savings, dividends from stocks, rental income, or royalties from intellectual property.

Understanding your Financial Freedom Ratio gives you a clear snapshot of where you stand on the path to financial independence.

It's your starting point to figure out how far you are from the ultimate goal: having your assets generate enough income to cover your expenses and beyond.

Tip 2: Everyone Has a Different Number.

Let’s consider two individuals, Tim and Tom.

Tim lives in Ipoh and spends about RM 5,000 each month, while Tom resides in Kuala Lumpur, where his monthly cash outflows are closer to RM 15,000.

Because Tim spends less, he needs fewer current assets and less passive income to reach financial freedom.

Even if Tim and Tom earn the same monthly income, Tim is likely to achieve financial freedom much faster simply because he spends less.

This brings us to a tip that often flies under the radar: “control your monthly cash outflows.”

The less you spend each month, the easier it becomes to achieve financial freedom. So, managing your expenses effectively is a crucial step towards financial independence.

Tip 3: Achieve Financial Stability First

Before setting your sights on financial freedom, it’s crucial to focus on becoming financially stable.

Financial stability means having enough current assets to cover 6-12 months of your monthly cash outflows.

So, if you’re Tim, living in Ipoh with RM 5,000 in monthly expenses, you’d need RM 30,000 to RM 60,000 in current assets to be financially stable. For Tom in Kuala Lumpur, who spends RM 15,000 a month, he’d need RM 90,000 to RM 180,000.

Having this safety net of current assets is vital. It shields you from the stress and anxiety that can come with life’s unexpected hiccups—things like a pay cut, layoff, unexpected repairs, or minor emergencies.

The most effective way to build up these current assets? Boost your monthly savings by:

- Increasing your active income.

- Controlling your monthly cash outflows.

Earning RM 10,000 a month makes it easier to save 30%, 40%, or even 50% of your income without sacrificing your lifestyle. So, increasing your active income is a key part of the equation.

However, be cautious. Many high-income earners fall into the trap of lifestyle inflation and mounting debt. The more they earn, the less financially stable they become. So, it’s not just about growing your income; it’s also about keeping your spending in check.

Tip 4: Invest in Income-Productive Assets

Let’s take Tim as an example.

Tim needs to earn RM 5k a month in passive income to achieve financial freedom.

Financial Freedom Ratio

= Current Assets / (Monthly Cash Outflows - Passive Income)

= Current Assets / (RM 5k a month - RM 5k a month)

= Current Assets / RM 0k a month

= Infinite Wealth (Financial Freedom)

So, how could Tim earn RM 5k a month in passive income?

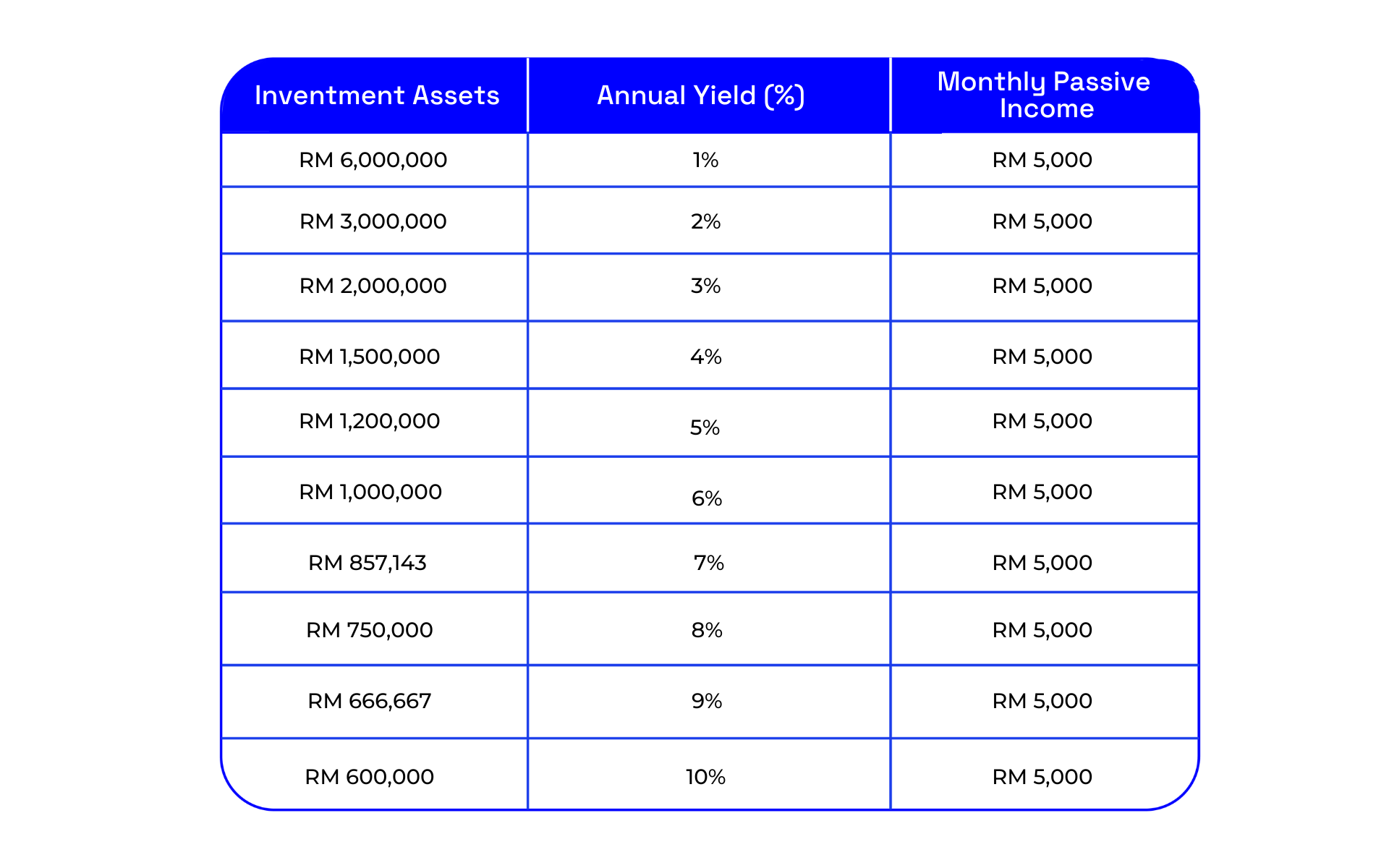

Well, he could choose not to invest and place all of his “current assets” into FDs that yield about 3% in interests per annum. If so, Tim needs to have RM 2 million in FDs to be financially free.

Assets x Annual Yield / 12 months = Monthly Passive Income

RM 2 million x 3% / 12 months = RM 5k

What if he chooses to build a stock portfolio that generates 6% in annual dividend yields? In this case, the amount Tim needs to become financially free would be much lower at RM 1 million.

Assets x Annual Yield / 12 months = Monthly Passive Income

RM 1 million x 6% / 12 months = RM 5k

As such, the higher the income yield we enjoy, the less capital/investment assets we need to enjoy financial freedom. Check out the table below:

So, why do we need to learn how to invest?

It is because the better we are at investing, the less capital we need to attain financial freedom.

Tip 5: How to Achieve Better Income Yields?

Take stock investing as an example.

Here, the context is own shares of high-quality businesses that increase earnings and operating cash flows for the long-term.

Long-term refers to a minimum period of 10 years as it is about the intention of keeping shares just like how one holds onto real estate for long-term rental income.

Let’s say, we have a stock: A Bhd. In Year 0, it earns RM 100 million and pays out RM 50 million in dividends. It issues 100 million shares.

Thus, A Bhd’s earnings per share (EPS) is RM 1.00. A Bhd’s dividends per share (DPS) is RM 0.50. At that time, you could buy A Bhd’s shares at RM 10 a share. Hence, your initial dividend yield is 5%.

Over time, A Bhd’s earnings kept increasing. So as its dividend payments to you as an investor. By Year 10, A Bhd earns RM 200 million and pays out RM 100 million in dividends. It issues 100 million shares.

So, its EPS is RM 2.00 and its DPS is RM 1.00 at Year 10. So, the dividend yield you receive at Year 10 is 10% based on your initial investment cost of RM 10. In that period, you would most likely enjoy some form of capital appreciation for A Bhd has successfully doubled its EPS and DPS in that 10-year period.

Hence, a practical approach to financial freedom is to own assets that could generate consistent growth in income over time, be it stocks or real estate.

The earlier we start investing right, the more income yield we earn over time, the less capital we need to invest to attain financial freedom.

For a start, if you want to know how I approach stock investing, you can check out this article:

Link: Stocks Criteria to Be On Your Watchlist

Conclusion:

In short, I believe we could attain financial freedom if we have a desire for it. Here, I’ll list down a set of “dos” that are helpful to fast-track us to financial freedom:

- Increase active income.

- Control monthly cash outflows.

- Invest in income-productive assets.

The earlier you start and the more consistent you are in repeating the above, the faster you will achieve financial freedom.

Remember: There is more to life than just participating in a rat race.