Navigate your risk with DCA

When it comes to investments, we always associate them with the risk of losses, which eventually become one of the reasons many of us refrain from getting involved.

Therefore, we kept our salaries, bonuses, and all other cash we received in the savings accounts as we deemed it safe and easily accessible.

However, here, in Malaysia, we are pretty fortunate as we have the option to put our hard-earned money into low-risk investments such as Amanah Saham Bumiputera (ASB) and Tabung Haji, which historically, manage to give us slightly higher returns than Savings Accounts and Fixed Deposits.

Why DCA?

Generally, when we talk about investment, there are three categories of risk: low, medium, and high, which offer low, medium, and high returns or profits, respectively.

As such, if you wish to seek higher returns than ASB or Tabung Haji, you may consider investing in moderate to high-risk investments such as unit trusts (with fluctuating prices), index funds, ETFs, and the stock market. However, you must also be prepared to bear the risk of capital loss.

Fret not; if you are really interested in having some taste of high-risk investment to earn a high return, there is a method known as Dollar Cost Averaging (DCA), which can assist you in better managing your risk. (This article will refer to DCA as Dollar Cost Averaging).

However, DCA is not a guarantee of profits or a way to avoid losses; instead, it is a method that can help to reduce risk.

What is Dollar Cost Averaging?

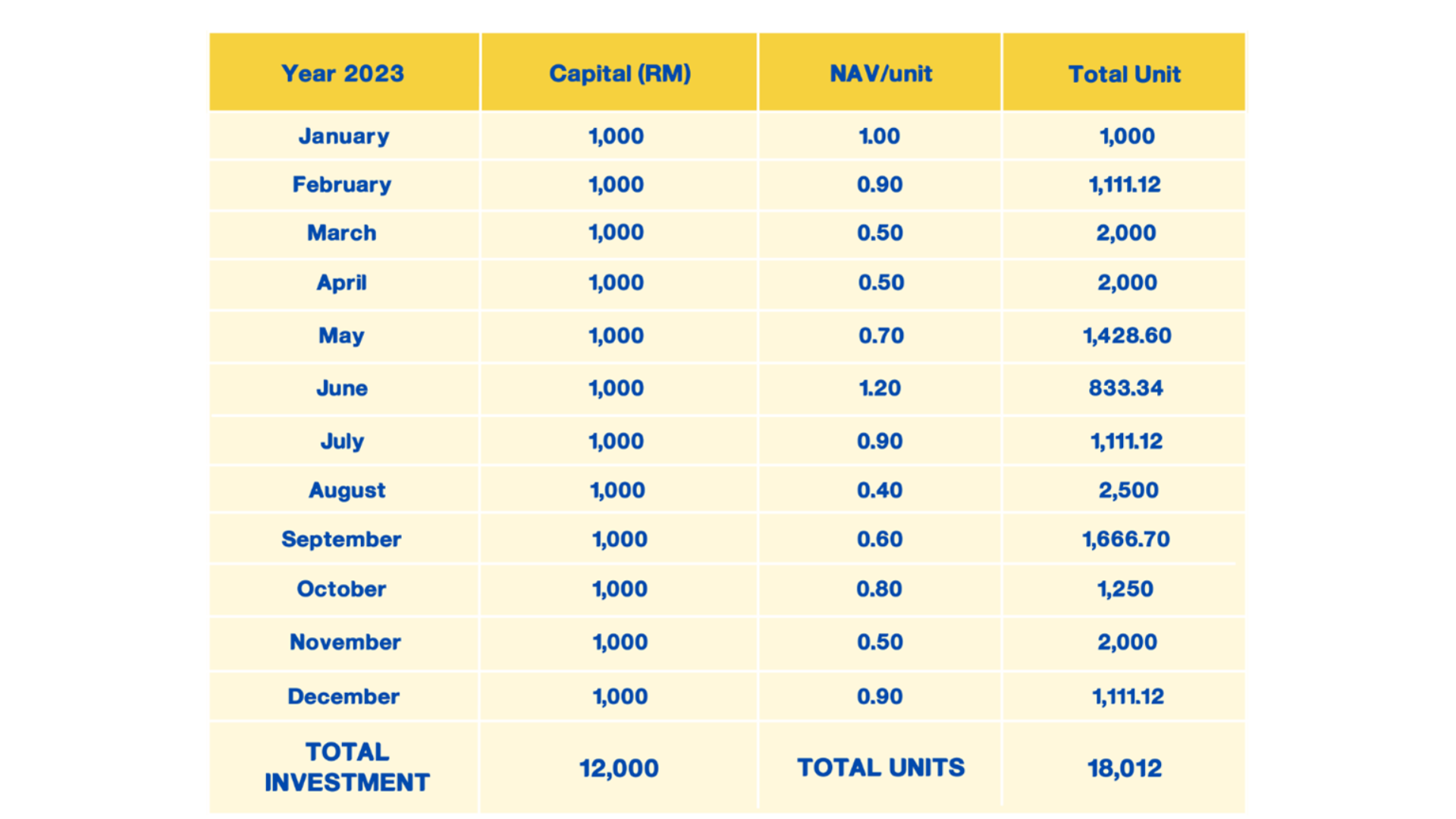

When you adopt the DCA method in your investment strategy, you will invest the same monthly amount. For example, you have decided to invest RM1,000 per month in an ABC unit trust.

For example, in January, you managed to secure 1,000 units priced at RM1 per unit, while in February, you managed to secure 1,111 units as the price at the time of purchase was 90 sen per unit. Below is your investment record for the year 2023:

Based on the table, with the same amount of investment monthly, you will get a different number of units depending on the price per unit. If the cost per unit is high for that month, you will get fewer units, and vice versa.

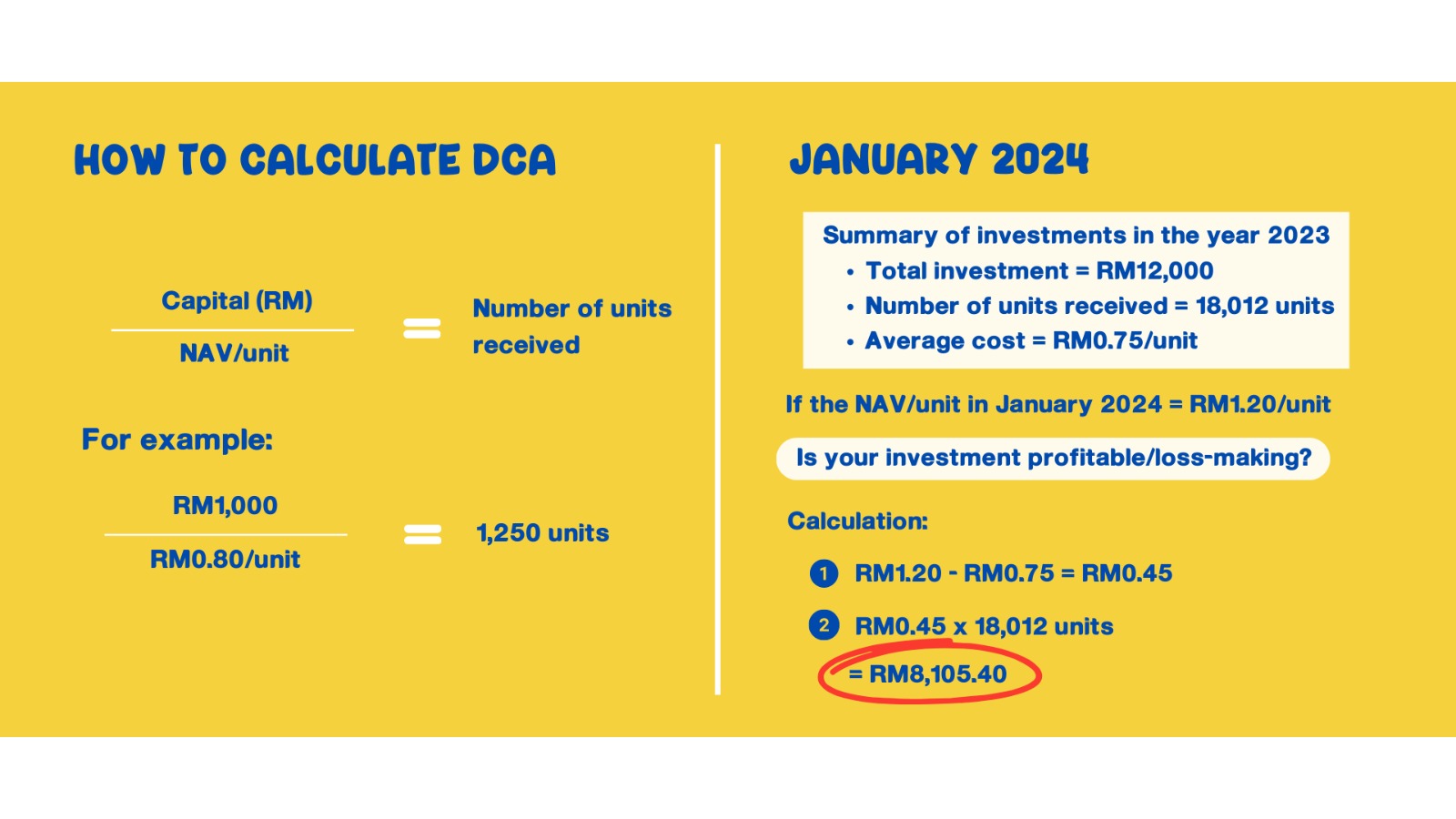

What will happen to your investment if the price per unit increases in January 2024? Will your investment make a profit or incur a loss? The calculations are shown in the table below:

To manage your investment easily, you can use systematic investment services such as standing instruction to enable you to invest consistently every month.

The Advantages of Using DCA

There are several advantages to using the DCA method in investing, especially for long-term investments. Let's explore the four (4) main benefits of DCA.

1. Dealing with Risks More Easily: If you invest a lumpsum amount at one time, the risk of incurring losses is also higher as the price fluctuations are complicated to predict and sometimes change without reason. Therefore, DCA is highly suitable for long-term investment as you do not have to worry about market fluctuations.

As such, you can manage your risk effectively as you can avoid making hasty decisions every time the unexpected happens.

2. Average Cost: By using the DCA method, you are buying at the average price per unit. When you are dealing with the average cost, you buy at a price that is neither excessively high nor too low in our investment, aiding in better control and long-term profit realization.

3. Managing Emotions: Fluctuations in stock prices can cause anyone to experience a heart attack, especially when the unexpected happens. This can be emotionally disturbing as you continually face uncertainty and worry about what will happen next week, next week, or next month. DCA can help you reduce emotional pressure as you already allocated a certain amount of money to be invested for a long time.

4. Suitable for Long-Term Investments: DCA is ideal for long-term investments as it utilizes the average cost. In the long term, stock price fluctuation will help investors realize gains.

The DCA method is suitable for managing risks if you are interested in investment instruments with moderate risk, such as unit trust, and high risk, such as the stock market, for the long term.

Who should use DCA?

However, DCA may not suit you if you consider yourself a short-term investor chasing high profits or already have the expertise and ample time to manage your investments.

On the other hand, if you are new to investing and want to explore moderate and high-risk instruments such as unit trust or the stock market, you can adopt DCA as your investment strategy.

In the meantime, continue to sharpen your knowledge and skills so that, moving forward, you can better manage your investment for higher returns.

Article Highlight:

1. Use the DCA method if you want to invest in moderate and high-risk instruments but do not have the necessary skills, knowledge, and time to manage such investments.

2. DCA helps you invest consistently every month for the long term without being influenced by emotions.

3. Set an amount that aligns with your financial ability so that you can remain consistent in your investment

4. Do not let emotions influence you in making investment decisions. As stock prices constantly fluctuate, DCA will help to reduce risks.