Build Financial Resilience, Own Your Dream Car

Build Financial Resilience, Own Your Dream Car

A car is often seen as a symbol of success and wealth, which is why many are willing to take on long-term financial commitments to realise their dream of owning a car.

When a loan is approved, many assume they are both eligible and capable. However, in reality there are many important considerations and analyses that should be made before committing to any long-term financial obligation, especially when the commitment is not a necessity.

Therefore, before committing to your dream car, consider the following checklist:

- Changes in life stages (next 3–5 years): Consider potential life changes such as marriage, starting a family, children growing older, or additional responsibilities that may increase the cost of living. A high car commitment may affect your financial stability.

- Debt Service Ratio (DSR) before and after purchasing the car: If the new car instalment causes your DSR to exceed 40%, reconsider your decision. Choose a car based on affordability and needs, not wants.

- Emergency fund equivalent to six months’ income: If you do not yet have sufficient emergency savings, avoid adding new debt commitments. Instead, start investing to build financial security.

- Impact on savings and investment commitments: Ask yourself: will this purchase reduce or stop your investment habit?If yes, reconsider. A car is a depreciating liability, while investments help build long‑term financial resilience and assets.

- Is this car a necessity or merely a status symbol? Answer honestly, as your response will have an impact on your long‑term financial well‑being, especially if the car is beyond your financial means.

Today’s Dream or Long‑Term Assets?

A dream car may provide comfort today, but wise financial decisions build long-term wealth and stability.

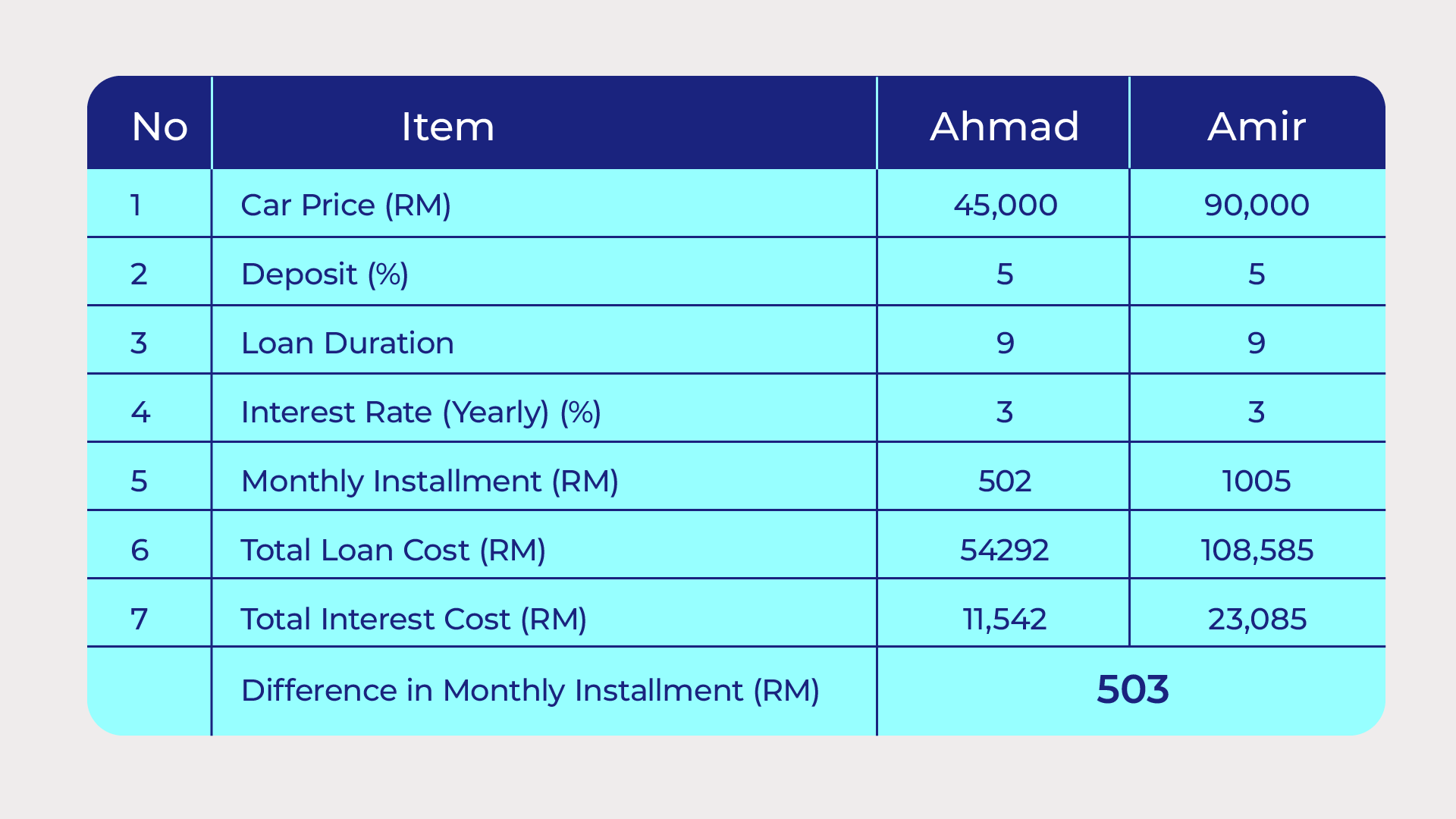

Imagine two individuals, two cars, and two very different financial realities. Ahmad chooses a car that meets his needs, with a monthly commitment of RM503. Amir, on the other hand, opts for a more expensive vehicle, committing RM1,005 each month.

Ahmad is financing a necessity, while Amir is funding a lifestyle driven by status and wants.

*Calculation based on the Car Loan Calculator available on ASNB Academy.

A car as a necessity will get you safely to your destination, just as a car as a symbol of status will do the same. The difference lies in making the wiser choice for better financial outcomes.

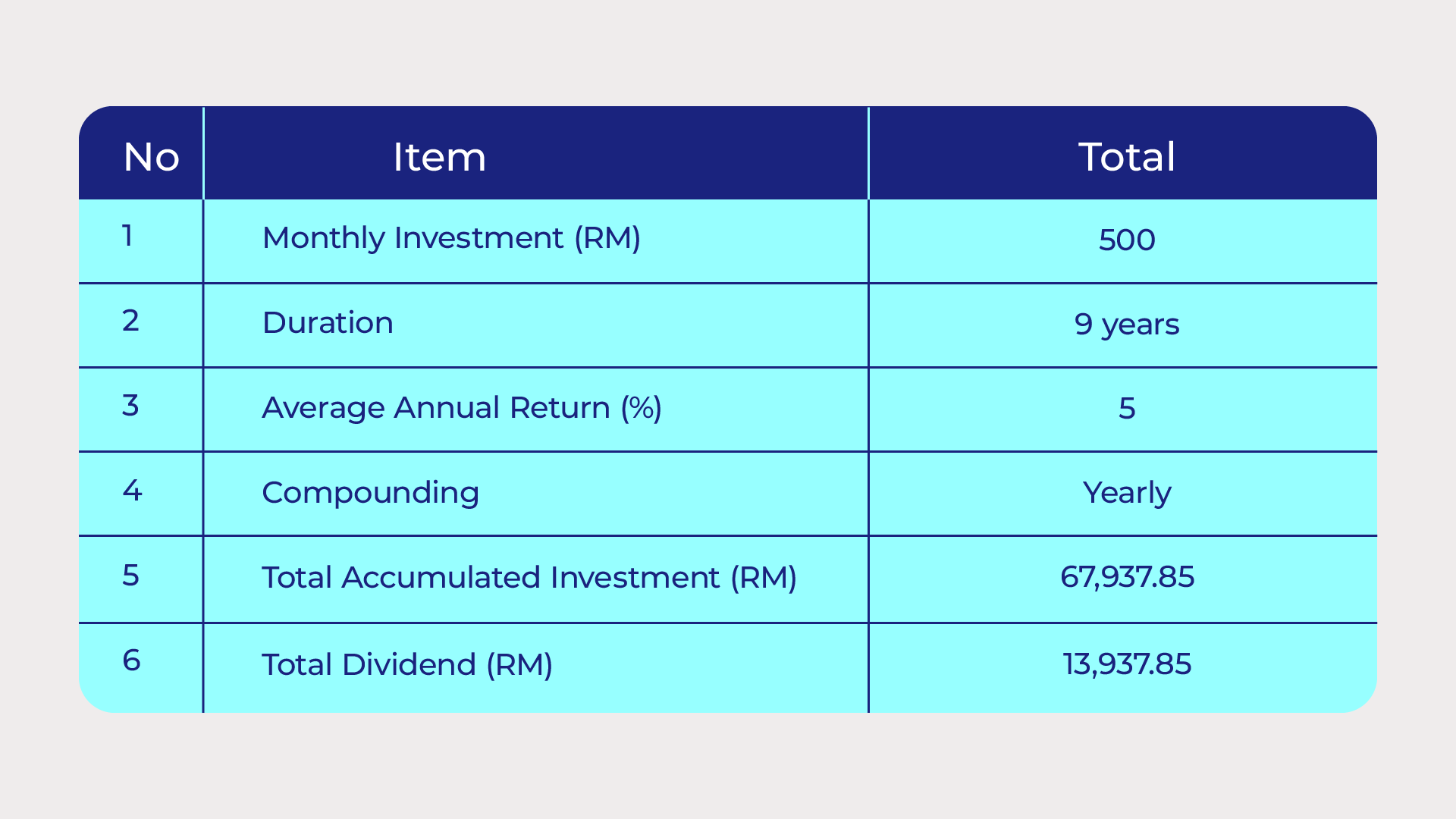

Now imagine if Amir had chosen a car priced at RM45,000 and set aside RM500 each month for investing instead.

Below is the projected investment value over 9 years:

*Calculations are based on the Regular Investment Calculator available on ASNB Academy.

By delaying a purchase driven by status and discretionary wants, Amir is able to build long‑term financial resilience through investing.

There is nothing wrong with Amir choosing to purchase a more expensive vehicle in the future when he is more financially capable. What matters is that the smart decisions he makes today allow him to build assets through investments.

A Smarter Strategy

A more prudent approach is to purchase a car based on one’s financial capability, while continuing to invest consistently with a minimum of RM500 in ASB or other ASNB unit trust funds.

Who knows, you may even drive home a BMW 320i M Sport offered under the ongoing Pandu Impianmu 2.0 campaign, which will run until the 31 March next year.

Other prizes on offer include a Proton e.MAS 7, six Perodua Bezza vehicles, five Petronas cards worth RM5,000 each, 20 accommodation packages (3 days, 2 nights at Hard Rock Hotel Penang and Hard Rock Hotel Desaru), as well as 100 Touch ‘n Go Reload PINs worth RM1,000.

The campaign is open to all ASNB investors. To participate, investors simply need to register and invest a minimum of RM500 in any ASNB unit trust fund to qualify for one entry.

To be eligible as a winner, participants must maintain a minimum Net Savings balance of RM500 throughout the campaign period.