Understanding Debt-To-Income Ratio

Managing our finances involves juggling various things, and one crucial indicator that plays a pivotal role in a person’s financial health is the Debt-to-Income (DTI) ratio. This metric provides a snapshot of an individual’s financial standing by measuring the relationship between their debt payments and overall income. Understanding the significance of DTI and how to manage it is fundamental to maintaining a healthy financial profile.

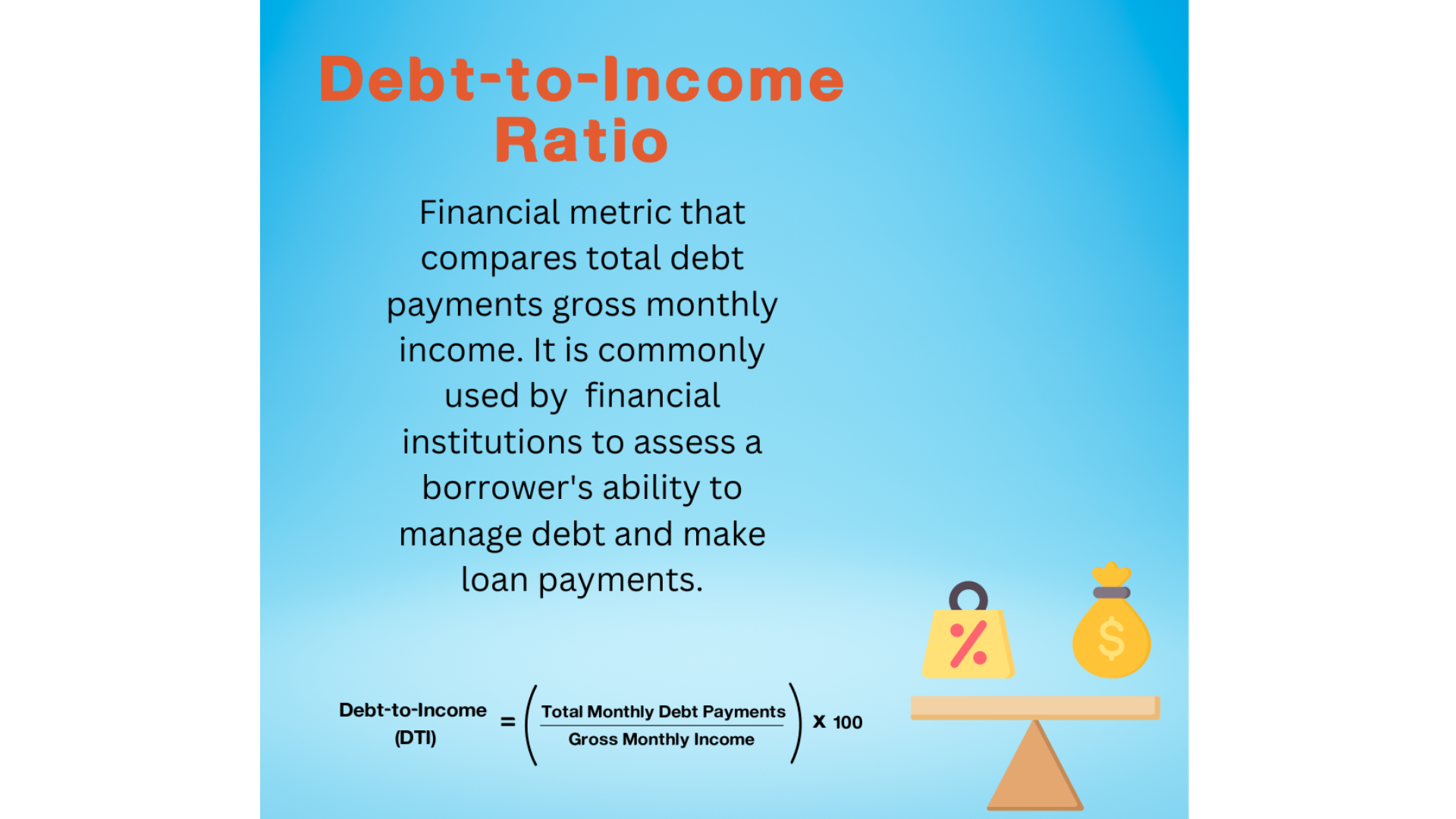

What is Debt-to-Income Ratio (DTI)?

DTI is a simple yet powerful financial metric lenders, namely financial institutions such as banks, use to assess an individual’s ability to manage monthly payments and repay debts. To calculate, you divide the total monthly debt payments by gross monthly income.

For example, Azman is thinking of purchasing another car and to do that, he will have to take on a hire-purchase loan. Before proceeding, he wants to assess his Debt-to-Income (DTI) ratio. His monthly financial details are as follows:

- Mortgage payment: RM 1,000

- Car loan payment: RM 500

- Credit card payments: RM 500

- Gross monthly income: RM 5,000

To calculate Azman’s Debt-to-Income ratio:

Add up monthly debt payments:

Total Monthly Debt Payments = Mortgage + Car Loan + Credit Card Payments

Total Monthly Debt Payments = RM 1,000 + RM 500 + RM 500 = RM 2,000

Calculate DTI Ratio:

DTI Ratio = (Total Monthly Debt Payments / Gross Monthly Income) x 100

DTI Ratio = (RM 2,000 / RM 5,000) x 100 = 40%

From the calculation above, we can see that Azman’s Debt-to-Income ratio is 40%. This means 40% of his monthly income goes toward his existing debt payments. This ratio suggests that Azman has a moderate debt burden compared to his income.

Therefore, Azman should be mindful of his existing debts, as his debt-to-service ratio has reached almost half his salary. Ideally, he should reconsider his decision to purchase another car as it will cause his debt-to-service ratio to increase and will also impact his cash flow.

Interpreting Debt-to-Income Ratio

35% and below : Generally, it is a healthy debt-to-income ratio, and we are all advised to maintain it within this range. Lenders also usually give an advantage to those with a ratio below 35%.

36% - 49% : This shows that you can still manage your debt. However, you are advised not to add to the debt and work to reduce it.

50% and above : With the debt burden equalling more than half of the income, this shows that you have a high debt burden, which makes it difficult for you to spend and invest. You are advised to immediately restructure the loan and take a cautious attitude in spending.

Why is Debt-to-Income Ratio Important?

1. Loan Eligibility

Lenders such as banks use this ratio to assess a person's loan eligibility. The higher the ratio, the harder it is for a person to get their loan applications approved.

2. Assessing Individual Financial Health

This ratio helps us manage the debt amount so that it does not exceed the suggested ratio. If you do the math and find your ratio exceeds the recommended range, you are advised to reduce your existing debt and not take out a new loan.

How to reduce your Debt-to-Income ratio

If your debt-to-income ratio is already over 40%, you should take steps to reduce debt. Here are some of the steps that can be taken.

i. Focus on paying off debt with the highest interest rates, such as credit cards. Reducing debt and using credit cards will indirectly help you strengthen your financial position

ii. You can restructure the debt by talking to the lender to reduce the interest rate or extend the loan term. If you feel your debt is too burdensome, you can seek advice from the Agensi Kaunseling dan Pengurusan Kredit (AKPK).

iii. You can supplement your income by doing a part-time job using writing, photography, or painting skills.

iv. Avoid adding debt, even if it's just debt like Buy First Pay Later because it will add a burden to your finances.

Debt-to-Income Ratio and Financial Stability

Maintaining a healthy DTI is vital in achieving financial stability. It impacts one’s ability to secure loans or credit and influences overall financial well-being. The debt-to-income ratio is critical in evaluating an individual’s financial health. Furthermore, a balanced DTI signifies that a person has a manageable debt load.

Ensure you regularly track and optimize your DTI for a healthier financial profile, which will pave the way for more favorable lending terms, lower financial stress, and enhanced overall well-being.

In essence, being mindful of DTI and taking proactive steps to maintain a balanced ratio is instrumental in achieving long-term financial security and peace of mind.

3 Key Takeaways

- Debt-to-Income Ratio must be less than 40%. If it's more, you need to reorganize your debt and avoid adding to the debt.

- Debt-to-Income Ratio will help you understand your current financial position, so always calculate this ratio before making any decision to take out a loan.

- The ability to control debt is very important for the well-being of life.