No Returns for Savings Account?

.png)

Many of us opt to leave our money in a Savings Account as we enjoy having the accessibility and convenience that come with it.

With the availability of debit cards and online facilities, having money in the Savings Account means that we can buy anything we want at any time, as long as there is money in the account.

As such, every time we receive our salary after settling all the bills and loan commitments, many of us leave our money in the Savings Account without realizing that, at the same time, we are missing the opportunity to make our money work for us.

We think that the amount of money is not significant to be invested, as investing involves the risk of losing the money if we are not knowledgeable enough.

However, do you know that here in Malaysia, we have the option to invest in a low-risk instrument, which, since its inception almost 40 years ago, has historically proven to have the ability to give out competitive returns?

The investment instrument is Amanah Saham Bumiputera, or fondly known as ASB.

While some of you may not be familiar with ASB, many have already reaped the benefits of investing, with the average return since 10 years ago being 6.2 cents per unit.

Understanding More About Savings Accounts

A Savings Account is a deposit account at financial institutions such as Maybank, CIMB Bank, Public Bank, and RHB Bank.

Many of us receive our salary via savings accounts, and these accounts usually become our main transaction gateway as they are easily accessible via ATM/debit cards and online banking.

Lately, online banking facilities such as money transfers, bill payments, investment, loan tracking, and some even help us track our spending, make money management much easier than it was 10 to 15 years ago.

However, a Savings Account yields low returns. For instance, in Malaysia, most banks offer interest rates below 0.5%, which is as good as no return. It is also prone to being attacked by scammers and hackers.

As such, leaving a large amount of money in the savings accounts is not advisable. We should only park the amount we need to pay for cost of living.

For instance, if we need at least RM3,000 in the account at all times to stay afloat, maybe we can leave around RM5,000 in the savings accounts.

The amount should be enough to pay for our daily and other expenses to live comfortably.

Understanding Amanah Saham Bumiputera (ASB)

ASB is a unit trust fund under Amanah Saham Nasional Berhad (ASNB). Even though ASB is a unit trust fund, it is offered at a fixed price, RM1 per unit, making it a low-risk investment instrument compared to other unit trusts offered at variable processes.

ASB offers an investment with unique characteristics such as:

• high liquidity – easy to withdraw,

• low-cost entry - minimum at RM10,

• easily accessible via more than 3,000 agents and branches nationwide,

• competitive return, and

• managed by Malaysia's biggest fund manager – Permodalan Nasional Berhad

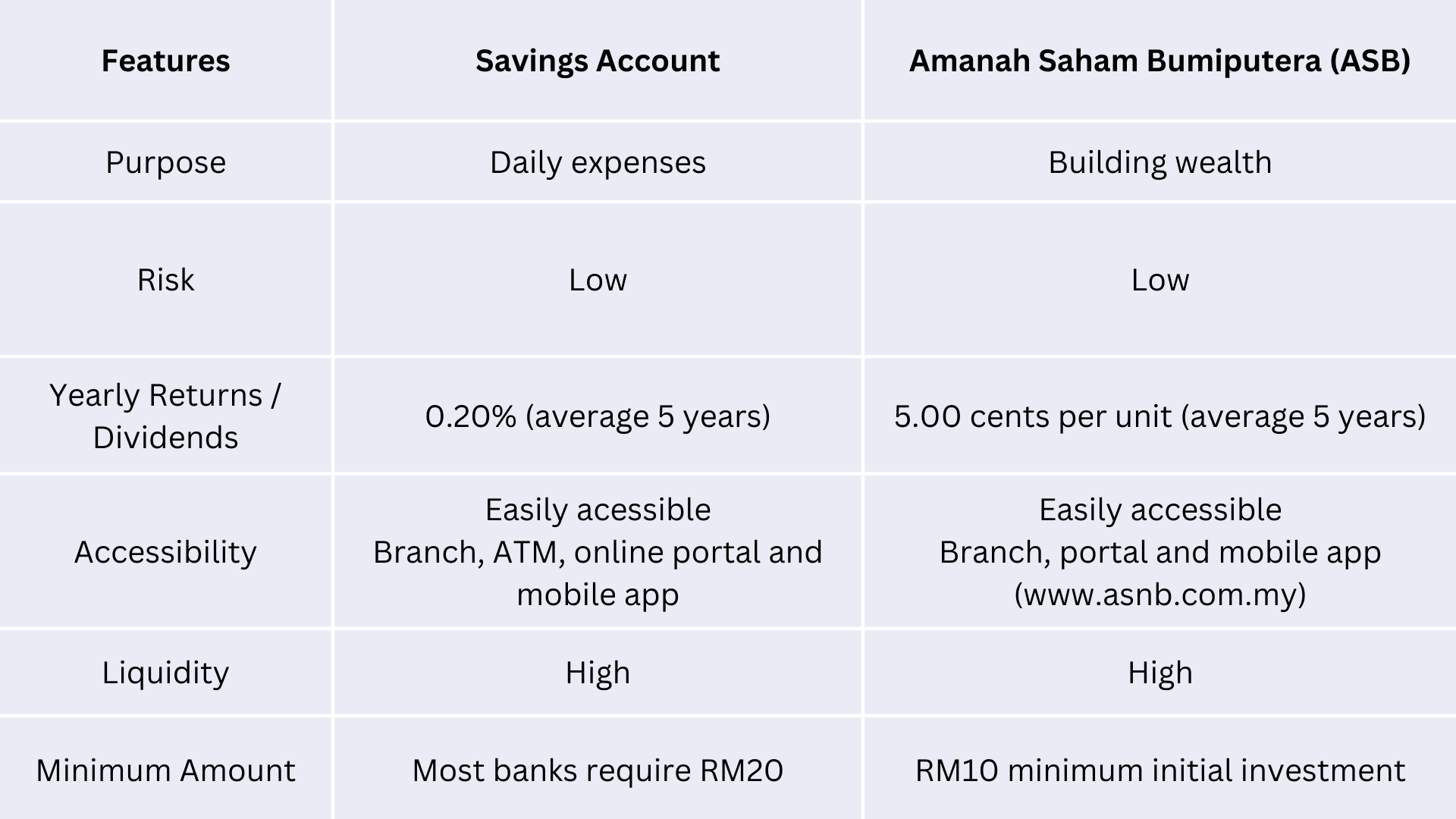

Savings Account vs ASB

The unique characteristics of ASB have confused many, and people assume that ASB and savings accounts are the same. What makes it even more confusing is that ASB is also offered via banking institutions such as Maybank, which leads us to think of it as another Savings Account provided by the bank.

As such, some of us do not even think of opening ASB, while those who have already invested treat ASB as a savings account, thus letting go of potential wealth growth offered by ASB via its competitive returns.

While ASB has consistently given out an average return of 5.00 cents per unit in the past 5 years, most savings accounts have maintained their yield of around 0.5%. However, to ensure that the money invested will grow substantially, you must invest consistently and avoid withdrawing your capital and dividend unless necessary.

Understanding the difference between ASB and savings accounts and taking advantage of investment in ASB will assist you in managing your money and investment better. Without worrying about losing capital, your money will keep working for you when you invest in ASB rather than letting it sit idly in a savings account.

As you already understand the difference between an ASB and a savings account, you should adopt the concept of 'invest first, spend later' in managing your income.

You are advised to invest up to 10 percent of your monthly income into ASB, and leave enough money in the Savings Account for your cost of living.

Remember that money left in a Savings Account will not generate much return and is prone to attack by scammers, while money invested in ASB will have more growth potential, helping us to beat inflation and build a fund.

Highlights

1. Put just enough money to pay for your monthly living costs and emergency needs in Savings Account.

Leaving a large sum of money in Savings Accounts will put you at a loss in terms of capital growth and fighting inflation.

2. ASB is not a savings account but an investment instrument. It is a fixed-price unit trust with unique characteristics such as low risk, high liquidity, low-cost entry, and so far, have managed to give out competitive dividends.

3. Invest First, Spend Later: Allocating a portion of your monthly income to an investment like ASB can help you to prioritize wealth accumulation over immediate spending.

By investing consistently, you can also safeguard against inflation and build a financial safety net for the future.